I wrote months about about a change in the residential market environment in the Austin metropolitan area:

This change actually began much earlier. It was noticeable in March of 2022, but it was hard to know how long it would last. Now, data through July of 2022 shows that we made a change that I believe will be healthy for Austin-area housing — a chance to build some inventory and calm price growth.

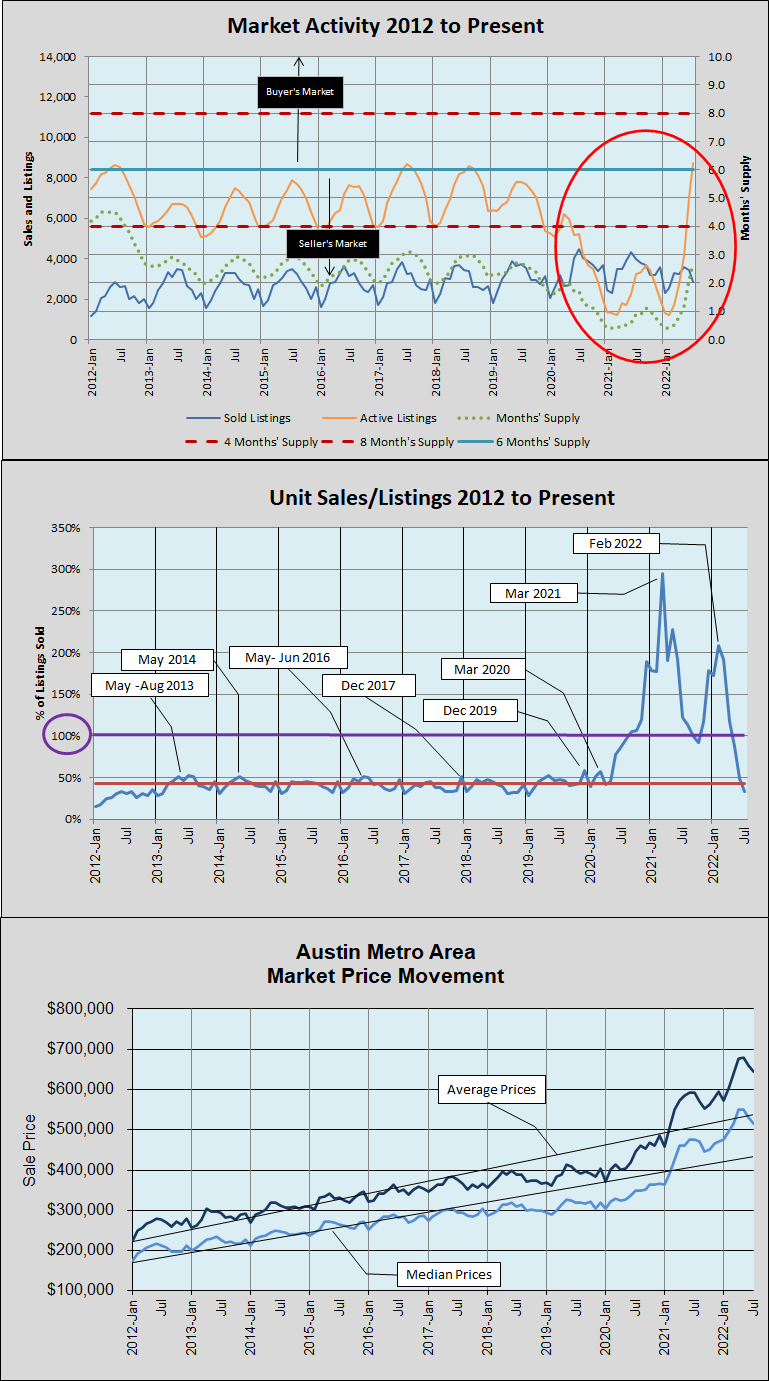

This snapshot of my market dashboard shows some important changes:

The top chart in that graphic shows the number of active listings and the number of homes sold for every month in this very long market cycle. The green dotted line shows how long that listing inventory would last if the same month’s pace of unit sales continued. That “Months’ Supply” metric has been very low throughout this market cycle — at or below three months for ten years! (For comparison, note that the industry has long considered six months’ supply to be “normal” or “balanced,” a level last seen in July 2011.) This dramatically low inventory has been the basis for the seller’s market conditions that we have all experienced during past 11 years.

The last two-plus years have been even more challenging. In the second chart above, you can see that from 2013 through most of 2020 the ratio of homes sold to homes listed stayed about 50%. The Months’ Supply line in the first chart shows that we were largely able to maintain seasonal inventories at that pace. But the second chart shows how significantly that changed in mid-2020, climbing from 42% to 97% from April to August. From September 2020 through April 2022, sales exceeded listings (except for a brief dip in late 2021).

That trend ended abruptly in March 2022, and the sales/listings ratio plummeted from 192% to 33% by July. Looking again at the top chart, the orange line shows the rapid increase in listing inventory, from 1,717 active listings in March to 8,709 in July! With that change, Months’ Supply was able to begin recovery, to 2.7 months in July.

Finally, the bottom chart shows the effect that pattern of supply-and-demand changes had on sale prices. Both average and median prices mostly flattened in 2018 and 2019, only to be pushed rapidly upward in 2021 and the first five months of 2022. The combination of reduced attractive inventory coupled with higher prices and rising interest rates caused prices to fall in June and July.

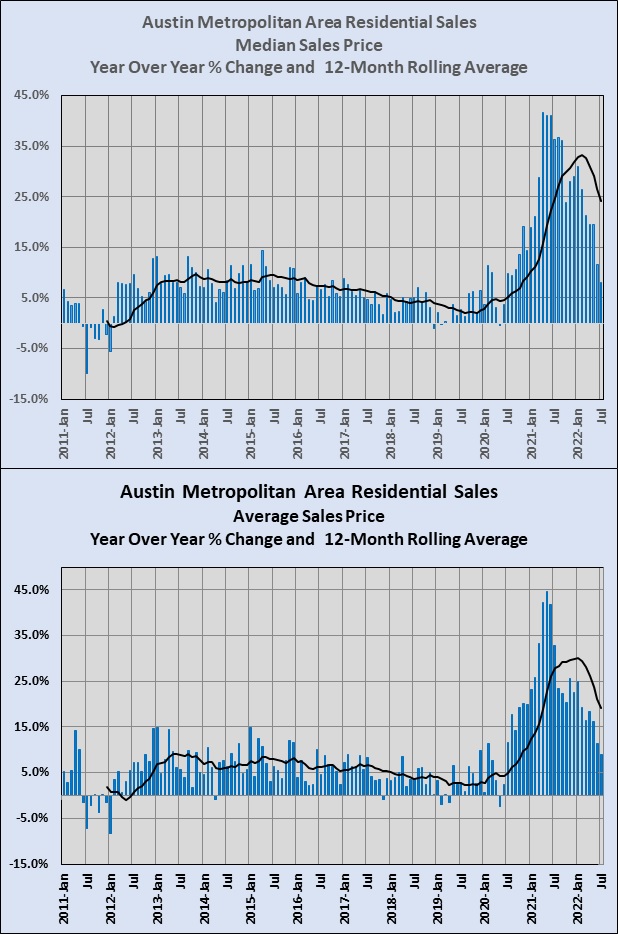

It’s important to know that even as sale prices declined month-to-month across the metro area, prices have still been climbing year-over-year:

What we have seen in recent months is a shift back toward what we have considered typical housing inventory during most of this market cycle, and annual price growth back toward the level we experienced before the pandemic. We may see price growth slow even more, but demand for housing in the Austin area shows no sign of abating, and by early 2023 I would expect to see the boom regain momentum, hopefully without the uncontrolled market frenzy we saw over the past two years.

Discussion

Trackbacks/Pingbacks

Pingback: A quick look back … and this market adjustment | Bill Morris on Austin Real Estate - September 4, 2022