It’s no secret that residential real estate has been HOT over the past ten years, and especially the past two years as housing inventories shrank across the U.S. In the greater Austin area, employers continue to move here and to expand, creating a supply-and-demand imbalance that is unmatched in other market areas. Market forces have driven inventories lower and prices higher — quickly!

There are indications nationally that local markets are in transition, with sales slowing and inventories growing somewhat. The Austin metro area has moved that direction over the past month or so too, but is it a lasting trend? The combination of higher prices and higher mortgage interest rates will inevitably affect some prospective homebuyers’ buying-power, and we have seen some buyers hesitating or dropping out and a few sellers hurrying to sell before the market shifts in favor of buyers. (That shift is not in view at this point.)

For perspective, consider: The real estate industry long assumed 6 months of housing inventory (the number of active listings divided by the number of homes sold in a month) to be “normal” or “balanced,” The Austin metropolitan area fell below that 6-months’ level in August 2010 and continued down to annual cycles that peaked at about 3 months’ supply in 2013 through 2018. The peak in 2019 was 2.7 months’ inventory, and supply fell to 2 months’ supply in 2020. Since November 2020 we have seen inventories almost every month between 0.4 and 0.9 months (12 to 27 days’ supply).

We have seen some changes recently, but strong demand continues, albeit slightly more tame than in 2021:

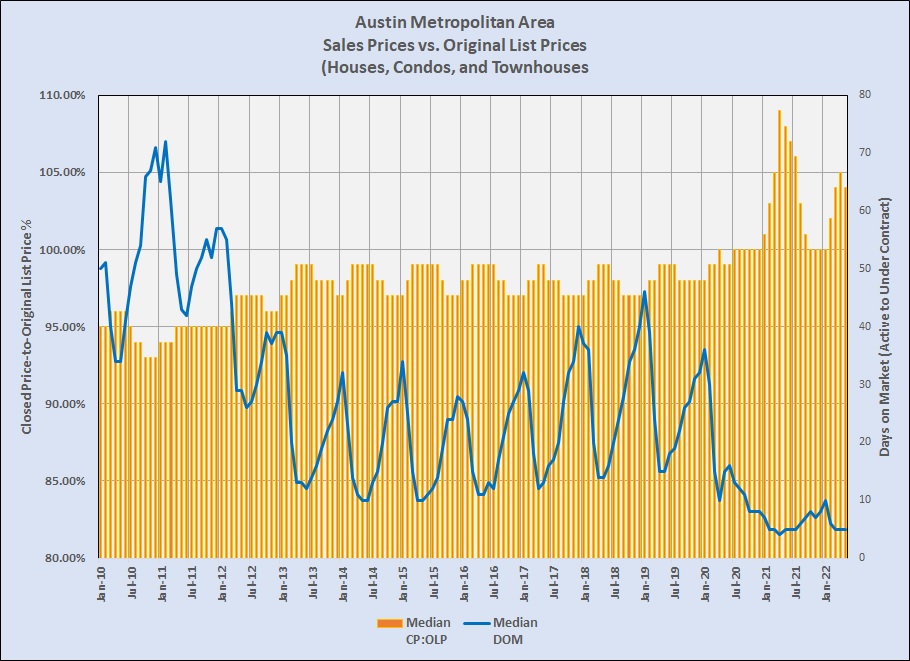

There was a flurry of activity in the first half of 2021, leading the median ratio of sales price to original list price to peak at 109% in April. We saw the same pattern so far in 2022, with the CP:OLP ratio peaking at 105% in April. Notice, though that the median time a sold home was on the market (Active to Under Contract) in March, April, and May of 2022 was still just 5 days, about the same as much of 2021.

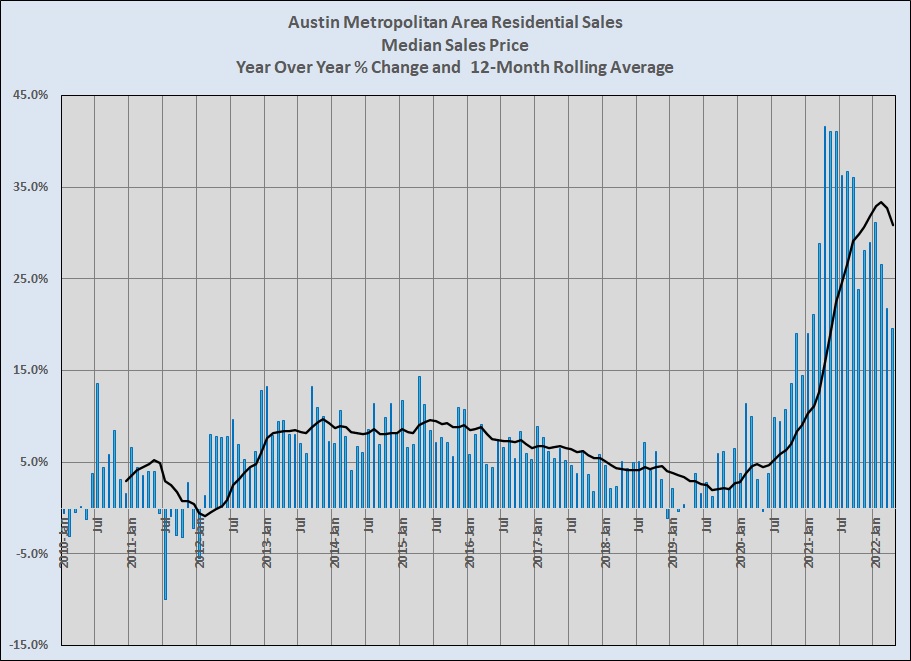

That market activity produced extreme changes in sale prices across the metro:

As mentioned above, things are somewhat calmer this year, but even though bidding wars aren’t generally as shocking as last year, the median price in April was still 19.6% higher than the previous April! The chart above uses final data as reported by the Texas Real Estate Reseach Center, and May data is still a couple of weeks away, but using MLS data it looks like May sales prices will show about the same 20% year-over-year growth.

At this point, we don’t have any indication that demand for housing in the Austin market will abate in the coming months. Sales are still moving quickly, with more buyers more price sensitive than they were last year. Housing supply remains seriously deficient to meet the still-growing demand. Many prospective home sellers remain reluctant to list and sell because of the environment they would face as buyers and because moving up could prove to be an expensive decision. In addition, home builders continue to face uncertainties in the cost and availability of both materials and labor. All of those forces together point to continued market inventory challenges and the upward price pressure that condition creates. Keep an eye on this, though. The national economy and election year volatility make this less predictable that we would like.

Discussion

Trackbacks/Pingbacks

Pingback: Market pause? | Bill Morris on Austin Real Estate - June 14, 2022

Pingback: Yes, the market has changed … ultimately for the better | Bill Morris on Austin Real Estate - August 28, 2022