I wrote the first draft of this post yesterday. Today I saw this article in REALTOR® Magazine, and it seems the perfect place to start: Mortgage Rates Slip After Fed Hike, But What’s Next?

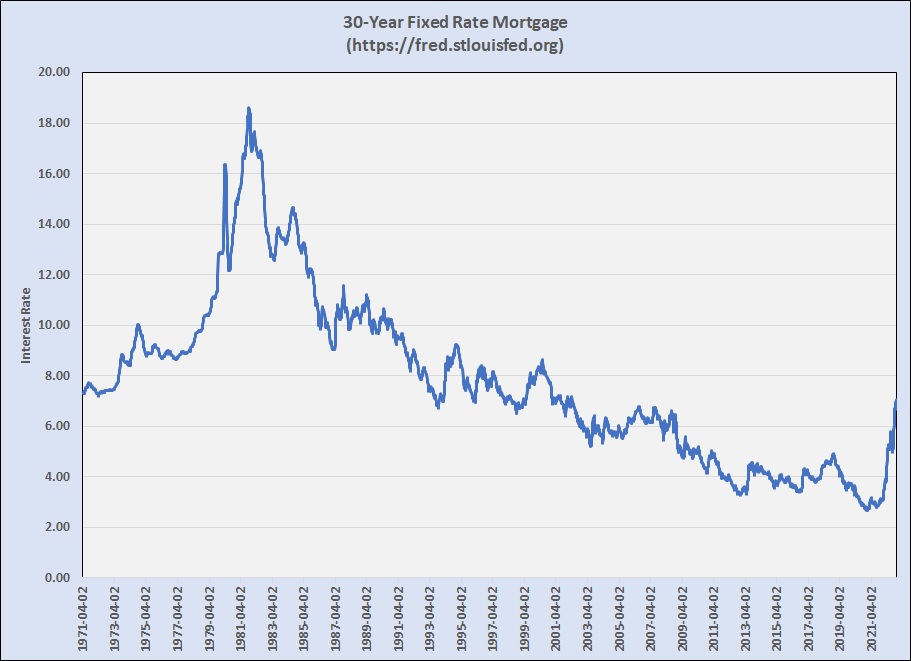

Mortgage interest rates have risen rapidly in 2022 — doubling from 3 1/2% in January to 7% now — and much is being made of how disruptive that is in the housing market. This change is certainly a factor in the market reset we have experienced this year (See The Market that was … and will be), but historical perspective is important, and it’s important to know that the Fed does not directly regulate mortage interest rates.

In the chart below you’ll see that the typical rate for a 30-year fixed rate mortgage loan now is about what it was in 2007-2009, but the most recent anomoly in the graph is the very low rates between 2011 and 2022. The 6% range experienced between 2003 and 2009 was very attractive at the time, and rates in every year before 2003 were higher — some MUCH higher! (Yes, that peak in 1981 was above 18% — and Americans still bought and sold houses during that time.

The news in recent months has frequently included dire warnings about the Federal Open Markets Committee raising “interest rates.” The rate those discussions typically cover is the “Fed Funds Rate” — what banks charge each other for overnight loans among themselves. There is no doubt that the Fed can set a floor for rates in the debt markets by increasing or decreasing banks’ basic cost of money, but market forces are also important influences. That definitely applies to the mortgage industry. In the chart below you can see that the general shape of the Fed Fund Rate graph closely resembles the mortgage rate chart above, but notice that the large bump in the Fed Funds Rate between 2004 and 2008 is barely noticeable in the mortgage rates above. The same is true in 2016-2020. Likewise, the deep valley and the peak preceding it in the mid-1970s barely registered on the graph of mortgage rates.

The more direct relationship in considering mortgage rates is the yield of 10-Year U.S. Treasury Bonds. That’s because investors in fixed-return instruments have alternatives — CDs, annuities, corporate bonds, municipal bonds, Treasury bonds, mortgage-backed securities, etc. Over a long period of history the shape of the 10-year Treasury bond graph looks much more like the mortgage loan rates than the Fed Funds rate, but offering lower yields. Compare the chart below to the first chart above:

By no means should we ignore what the Fed does, but I keep hearing that the Fed is pushing mortgage rates up. The Fed does not do that, but demand for housing and for loans to facilitate buying and selling homes can drive home prices and mortgage rates up. We still have a severe imbalance between the supply of homes and the demand for them across the U.S. Mortgage lenders survive by capturing their share of the loans made to home buyers, and lower interest rates can be one of the ways they compete. Most recently, mortgage rate increases have matched the Fed’s moves, but they are bouncing back from unsustainably low loan costs of the past couple of years. We got spoiled in 2020 and 2021, but moving back toward “normal” with mortgage rates and housing supply — painful as the process may seem now — will be positive in the end, and will allow us to live and work in more balanced market conditions for years to come.

The linked article at the beginning of this post offered two alternatives for the coming months — mortgage rates stabilizing, or continuing to rise. I won’t make a prediction myself, but as you watch or read the news you should know that what the Fed does won’t solely determine what happens in the mortgage business. Mortgage rates are not likely to decline, but they won’t necessarily follow the Fed’s upward moves either. I’ll keep you informed here.

Discussion

Trackbacks/Pingbacks

Pingback: Austin resale market shift 2022 | Bill Morris on Austin Real Estate - January 17, 2023