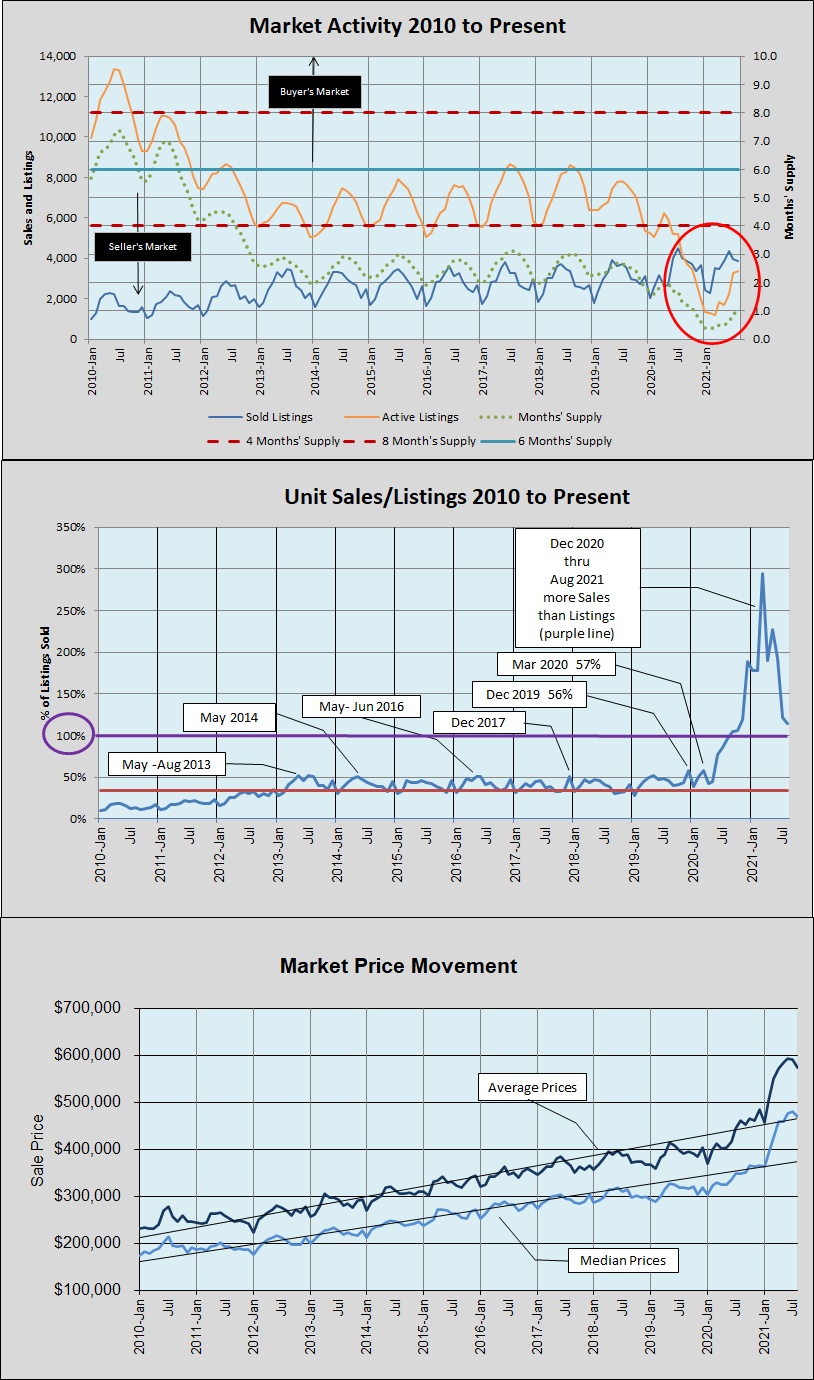

Last month I updated my market dashboard with refined data through July 2021 (Market Dashboard – a broad update). In that post I told you that the ratio of unit sales to listings had come down sharply from March to July, and that the pace of price increases was flattening. The general trends continued in August:

With this update, the August gap between listings and sales is narrower than it was in July, and for the first time in 2021, average and median prices visibly declined year-over-year. (And both average and median prices declined from July to August this year.)

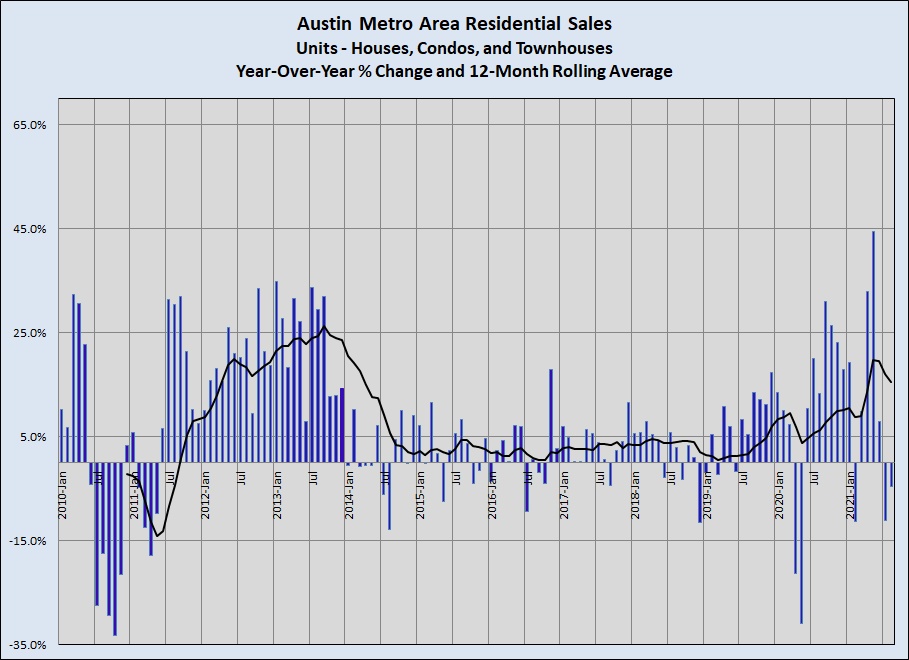

This chart highlights the year-to-year decline in unit sales:

As recently as May 2021 the number of homes sold was 45% higher than a year earlier. June 2021 unit volume was up only 8% year-over-year, and both July and August saw month-to-month and year-to-year declines in unit sales.

Note that in August, residential listing inventory was still just one month’s supply — up from a low of 0.4 month in the first three months of the year but far below a “balanced” 6-months’ supply. But with buyers frustrated by months of frantic bidding wars and concerned about how fast prices were rising even that small adjustment in inventory calmed demand and price growth.

The median sale price in August was up 35% from the same time last year, but the pace of price growth declined for two consecutive months. The median sale price in August was actually lower than July of this year and a full 10% lower than February, March, and April.

I closed my last post on this subject by saying that we won’t see a linear return to “normal.” According to Fortune magazine (What to expect in the 2022 housing market), quotes economist Skylar Olsen saying that the national housing picture 2022 will show “… the tides turning, with the market becoming “friendlier” to buyers.” But the Fortune article continues “… experts don’t believe the rise in inventory will push down home prices—those are still expected to keep rising.”

Keep in mind that Texas remains one of the most extreme sellers’ markets in the United States, and Austin is the most challenging metro area in the state. Adding resale listings to our inventory will remain gridlocked to some degree because prospective buyers who want to stay in the area must face the issue of finding and buying their next home at current prices. The key to adding substantial inventory will remain in new home construction. I will write soon about that part of our puzzle, but builders are making some progress in the face of considerable challenges.

Discussion

No comments yet.