These recent headlines caught my attention:

As Americans pay more for rent, landlords get some relief

Hot housing market pushes Austin rents to all-time high

The first article discusses national trends for apartment rent, and I agree that there is upward pressure on that segment of the larger residential rental market. As sale prices of residential properties have escalated in recent years, landlords have of course tried to keep up. In the process some prospective tenants who wanted lower-density properties were squeezed into the apartment market. The AP article says:

“Rising apartment rents represent a shift from earlier this year, when they weren’t growing and vacancies kept rising. That changed in the spring when pandemic-related restrictions were loosened following a ramped-up distribution of coronavirus vaccines. Since then, an improving economy and job market have helped stoke demand for rental housing.”

It’s important to note, though, that the “national average effective rent” in the 2nd quarter of 2021 rose 0.6%, and that while vacancies are about in line with the 10-year average, there are still more vacancies than before the pandemic began. “Freddie Mac projects U.S. apartment rents will rise 2.5% this year, while the vacancy rate slips to 5%,” AP adds.

The second article clearly focuses on the Austin area, and includes important data about increases in average apartment rents across the metro. It says that the average rent “… is now $1,442 a month, up from $1,278 in July 2020 and $1,311 in July 2019, according to the latest market report from AparrtmentData.com.” That’s a 12.8% increase from 2020 to 2021 (after a rent decrease from 2019 to 2020). The same article, however, also points out that the median sale price of a home in the Austin area in May 2021 was 33.6% higher than the same month in 2020.

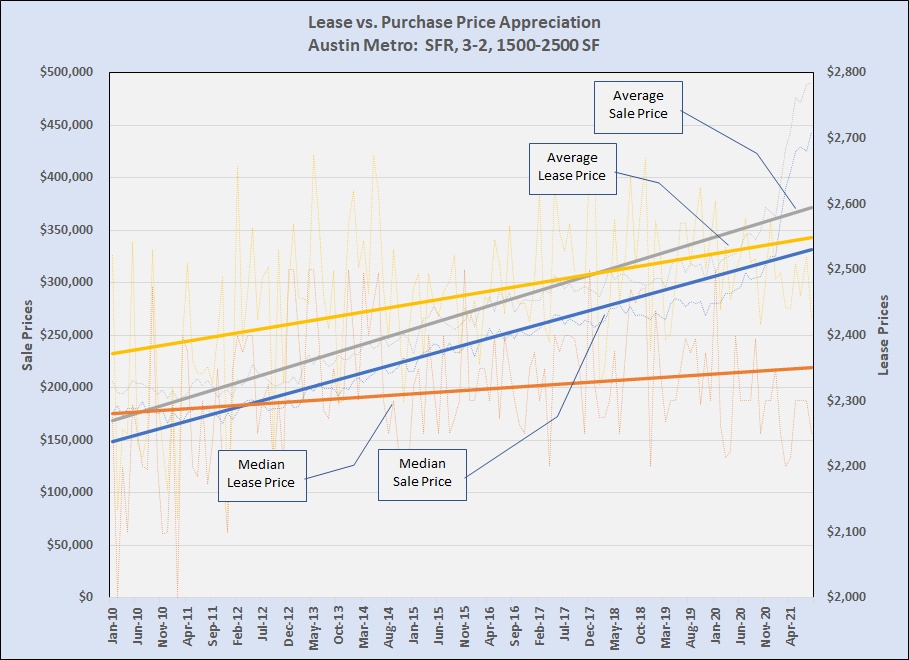

Over the past couple of years I have written about the vast difference between price escalation in the for-sale and the for-lease segments of our housing market. (Investing in Austin real estate, August 2019 and Investing in Austin?, July 2020). Using trendlines and moving averages, those posts showed that rent increases have not kept up with sale price increases. That has challenged new investors, and the gap has become vastly more challenging in 2021.

For easy comparison with those earlier posts I based this year’s update on sales and leases of 3 bedroom-2 bath single family homes, 1,500 to 2,500 SF in size. The specifics in different market segments and geographic market areas vary, but this is a fair proxy for the bulk of our non-apartment rentals. Here are the same types of graphs that were the focus of my previous analyses:

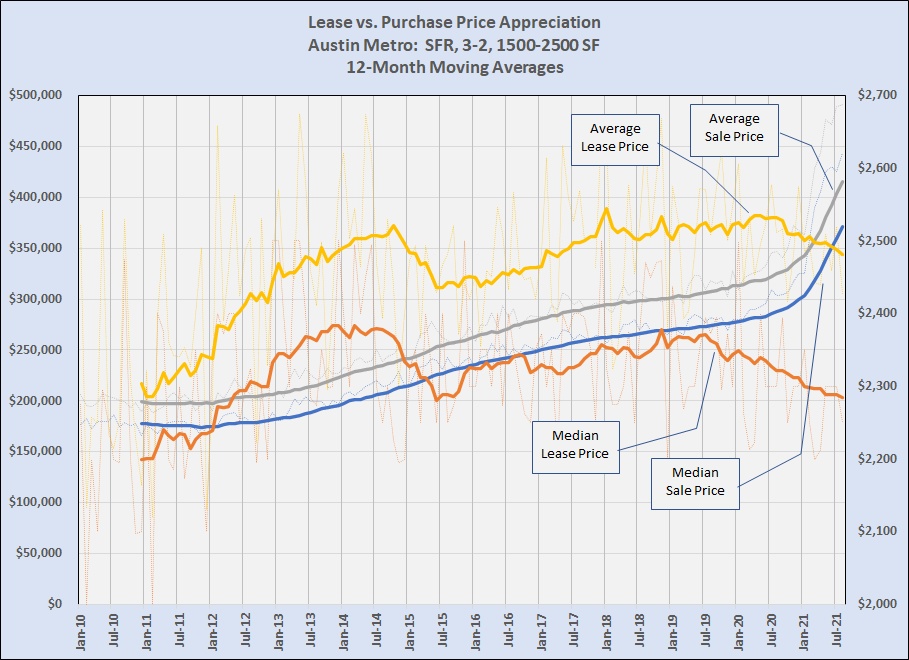

The linear trends still show the faster rise in sale prices versus leases, but this year’s look at 12-month moving averages is very different in two ways: (1) year over year increases in sale prices soared between mid-2020 (after my last post on this subject) and mid-2021; and (2) year over year rent prices fell during the past two years, with median rents now back to mid-2015 levels.

One more chart shows that even more starkly:

Yes, the blue and gray bars show the pace of change in sale prices in the selected market segment. The orange and yellow bars show what has happened to rents. July 2020 is when the changes diverged significantly.

I’ll write separately about how our for-sale market seems, for now, to be calming somewhat but it’s clear that closing the gap will take some time, especially as experienced landlords cash out, reducing the supply of for-rent properties at the same time that many investors wishing to expand will either stay on the sidlines or accept much lower returns on their investments than previously. For now this looks good for renters, but it bears watching.

Discussion

No comments yet.