Over the past week I have been exploring the effect of Covid-19 and various stay-at-home orders on the residential real estate market in the Greater Austin area. Obviously, our regional economy has been brought to a virtual standstill along with most of the developed world. As a foundation for my discussion later, here is a good look from CNBC at the difference between this situation and previous economic downturns, including the Great Depression:

The coronavirus recession is unlike any economic downturn in US history

These snippets from that article are worth thinking about:

Federal Reserve Chairman Jerome Powell: “I would point to the difference between this and a normal recession: There is nothing fundamentally wrong with our economy.“

Former Fed Chairman Ben Bernanke said our situation now is more like a natural disaster than to the Great Depression, which “… lasted 12 years, and it came from human problems, monetary and financial shocks that hit the global system,”

Adam Posen, president of the Peterson Institute for International Economics: “The most important difference is this comes out of the real economy, something biological, and people’s choices with responding to that, and not out of financial excess or financial speculation.”

Clearly, the short-term economic impact of Covid-19 has been severe and will continue to be for some time to come. In my real estate practice during this time, though, I encountered a couple of things that I found interesting and felt the need to look into:

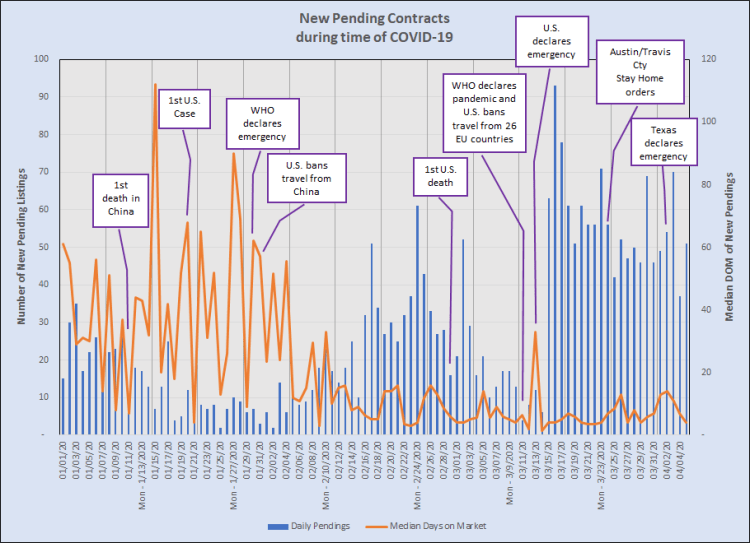

First, there was a noticeable surge in new purchase contracts in the weeks immediately following the United States’ declaration of a national emergency:

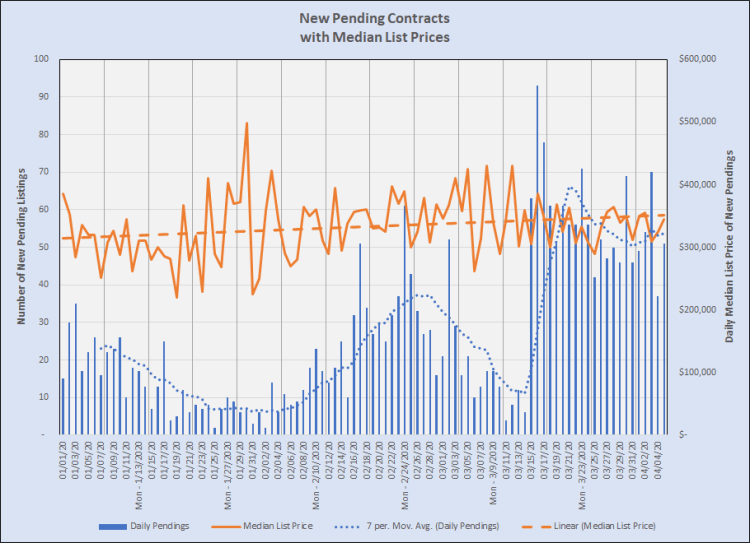

From mid-January through the first week of February, the pace of new contracts was relatively low as our market absorbed aging inventory. That was also largely lower priced inventory, with daily median prices frequently at or below $300,000:

That period was likely dominated by bargain-hunting investor-buyers and pre-approved owner-occupants who began their searches before the holiday period and were frustrated by the lowest inventory we experienced in all of this seven-plus year market boom.

There was a brief surge in new contracts in the second half of February, but it had largely ended by the time of the first reported death due to Covid-19 in the U.S. It stayed low until two days after the national emergency declaration, then soared March 15 and 16. By that time, daily median prices had grown from January’s $300,000 – $320,000 range to $350,000-plus. Buyer activity during that period was truly frenzied in mid-range market segments.

The second trend I encountered was a steady stream of new listings beginning in late February and continuing through March and into April. As our stay-at-home orders slowed new showings and purchases, those listings kept coming:

That chart shows the same daily sales as the other charts above, but it also includes the number of new listings that came on the market each day. The yellow line shows the “net new inventory” that resulted by April 5 — 2,331 active listings. That is about 3/4 of an average month of sales in 2019.

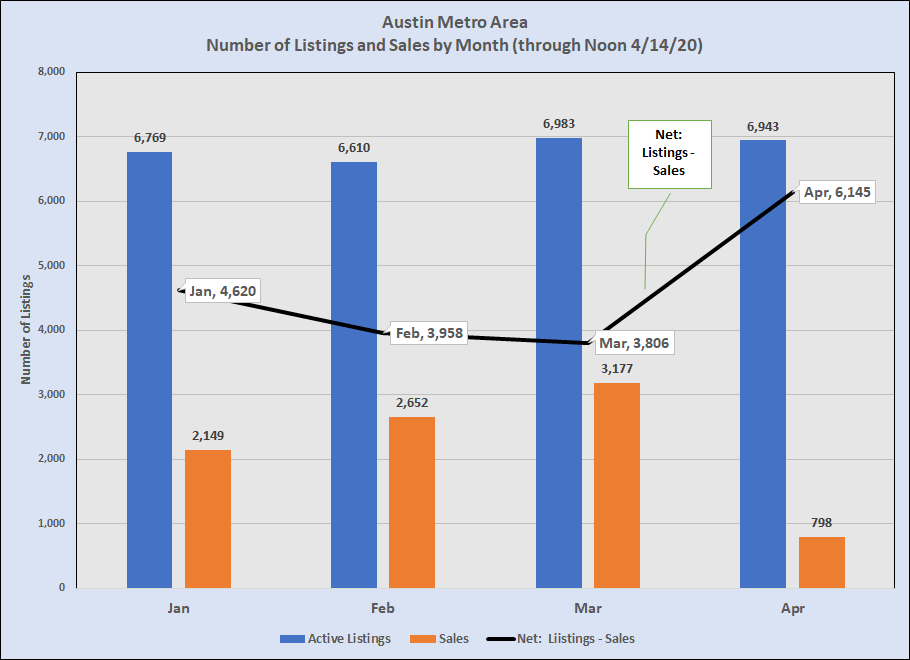

That new inventory was in addition to listing inventory we already had. Compiling all of this into monthly totals, here’s where we are now:

Listing inventory in March was just under 7,000 units, and March sales were almost 20% higher than in February! As I write this at noon on April 14, there were only 798 closed sales this month, and the net of listings minus sales is up 2,339 compared to March.

Note that the orange bars in that graph are actual closed sales, contracted 30 days or so earlier. Also note that we only have half of April accounted for. The surge in new contracts in late March should accelerate closings in late April, but whether it can match March performance remains to be seen.

Nonetheless, we will have significant inventory available as plans develop to reopen the regional economy, possibly later in May, and I know personally that there are more would-be sellers and pre-approved buyers on the sidelines now, waiting for reentry into the market.

I agree with the high-level opinions from the CNBC article I cited at the top of this post and the confidence they represent, and I remain optimistic about our local/regional real estate sector getting off to a quick re-start as soon as that becomes possible. Regaining buyers’ confidence in shopping and and sellers’ confidence in opening their homes, all without jeopardizing health, will be key.

Discussion

Trackbacks/Pingbacks

Pingback: Strong March performance … Next? | Bill Morris on Austin Real Estate - April 22, 2020