Earlier this year I wrote about the distribution of sales prices in Central Texas (Home Prices in Austin and More on Austin-area Home Prices). Since housing affordability is so often a topic of conversation these days, I want to offer some thoughts on that subject now.

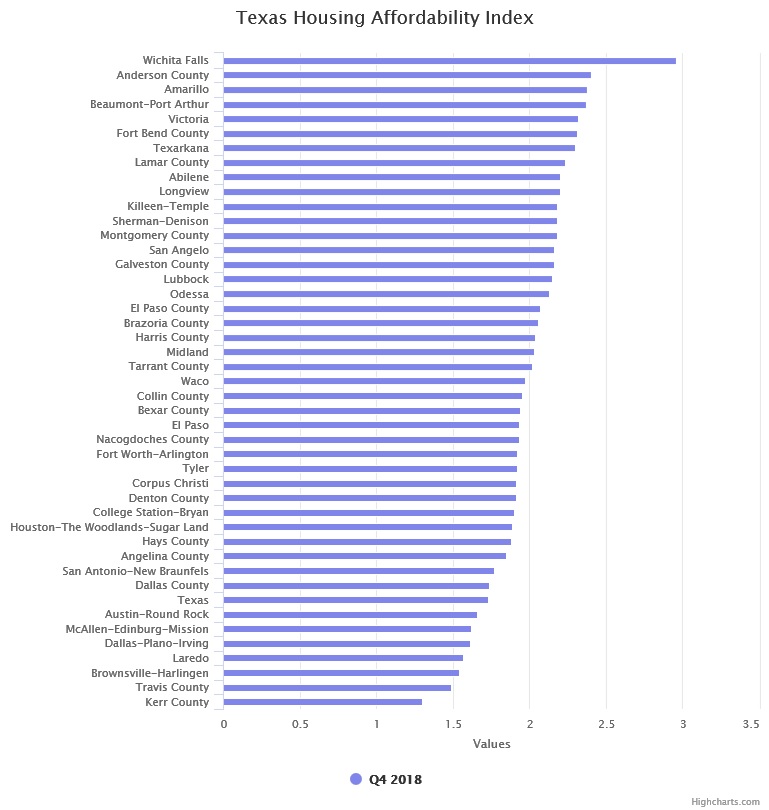

As a starting point, this chart shows the relative affordability of the Metropolitan Statistical Areas in Texas:

You’ll find the Austin-Round Rock MSA seventh from the bottom, with a THAI of 1.59. Since a THAI of 1.00 indicates that the median income in a location is just enough to qualify to purchase a median-priced home, our 1.59 rating means that the median household income in our area is 59% more than needed for that purchase.

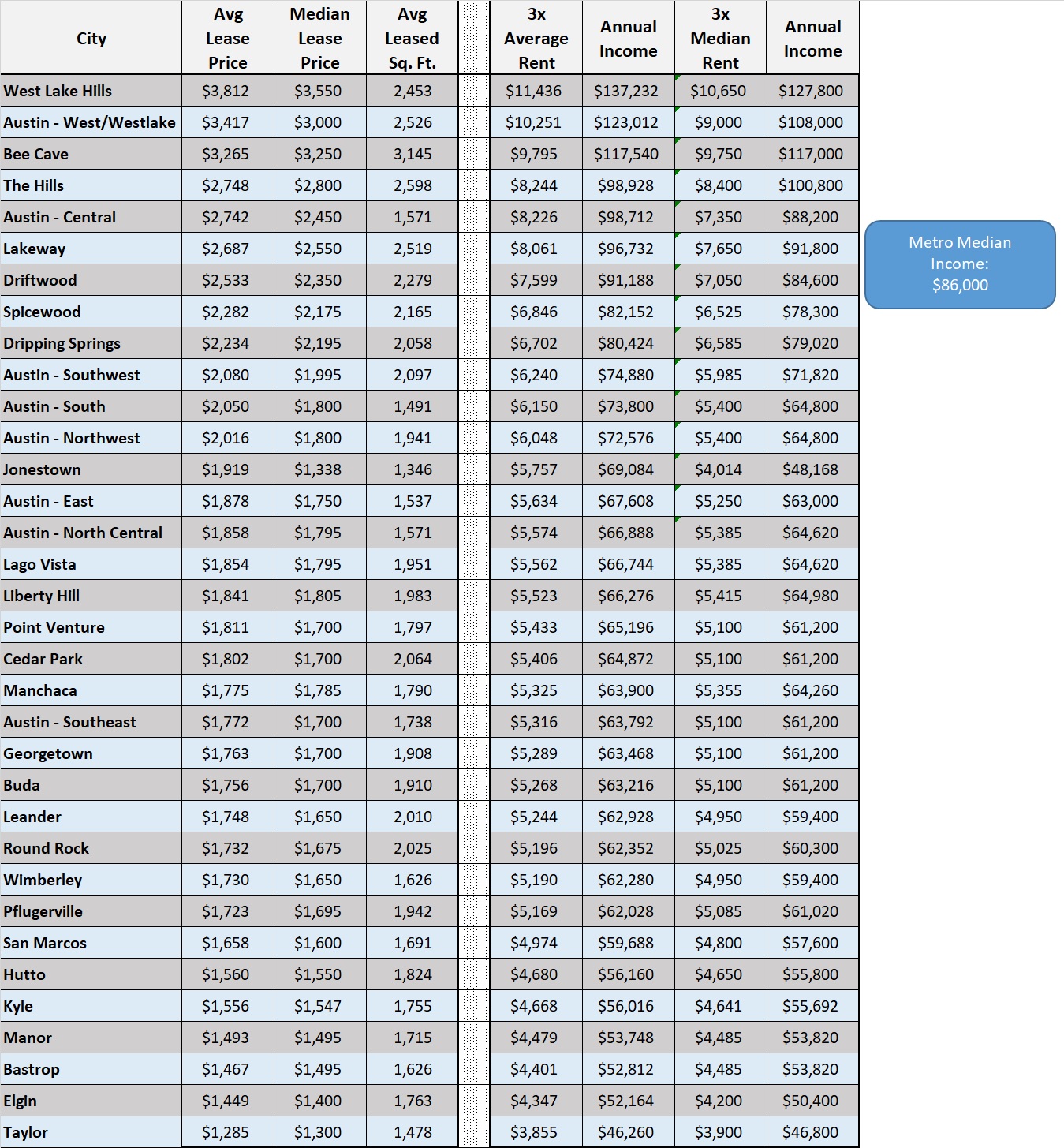

Now here’s how the median income in our area stacked up against median sales prices from last year:

Notice that my calculations required the buyer’s monthly mortgage payment (PITI) to be 30% or less of gross household income. That’s because I assumed that many/most families have other debts besides their mortgage. The THAI calculations allows the mortgage payment to account for all of the allowable debt-to-income ratio. With that explanation, you can see that median income in our area could afford housing at or below our 4Q ’18 median price of $300,000, and a little higher (Cedar Park, Liberty Hill and below in that chart).

However, that calculation assumes that buyers can assemble a 20% down payment. That is a challenge for many, and home prices continue to climb (albeit more slowly than earlier in this market cycle). For those who have income but inadequate savings, renting remains an important alternative. This chart shows where this part of our population can live affordably:

A frequent requirement by residential property managers in the Austin area (for 1 to 4 family properties) is tenant income at least three times the monthly rent. The right-hand columns in the chart above show those calculations, and you can see that renting housing is much more accessible for many Austinites than buying.

That is largely because permits were approved for almost 60,000 dwelling units in 5-plus family structures between 2012 and 2017. That growing supply has slowed increases in apartment rentals, which in turn retarded rent increases in the 1-to-4 family space. Rents simply have not been able to increase as quickly as sales prices.

Housing affordability is a real and growing concern in Austin and around the United States. Moreover, Austin and Central Texas rank among the least affordable metro areas in Texas. Buying a home here can certainly be a challenge at or below the middle of the market price range. Adding inventory in that part of the market is a critical issue, and one that is largely being missed by home builders. Predicting a real change in that situation soon would be foolish, but so far we continue to accommodate most new Austinites’ housing needs — buying or renting — with location/commuting time and cost being a key trade-off.

Good stuff.

However shouldn’t affordability be taken in context with job creation? Otherwise it’s not a true comparison in this analysts view…

Thoughts?

MS

Posted by Mark Sprague | May 28, 2019, 3:02 PM