It’s that time of year again … the traditional Spring/Summer residential sales season, and the Austin-area market remains challenged by very low housing supply. Even as rapid population growth continues (still about 150 people per day), the number of houses, condos, and townhouses eked out just 2% growth in 2018 compared with 2017.

The supply-and-demand environment I have told you about for years remains:

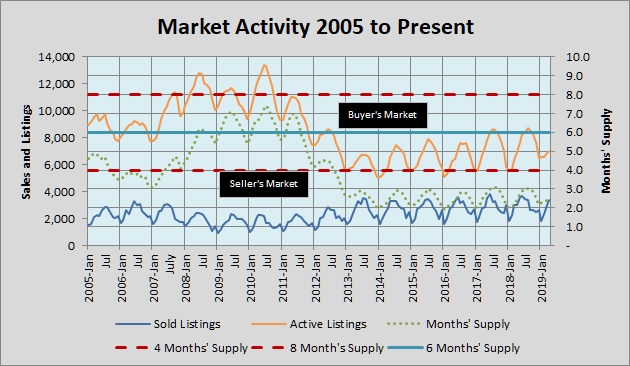

Compared to 6 months’ “balanced” listing inventory, we are entering our seventh year with supply at or below 3 months. And that drives strong sales:

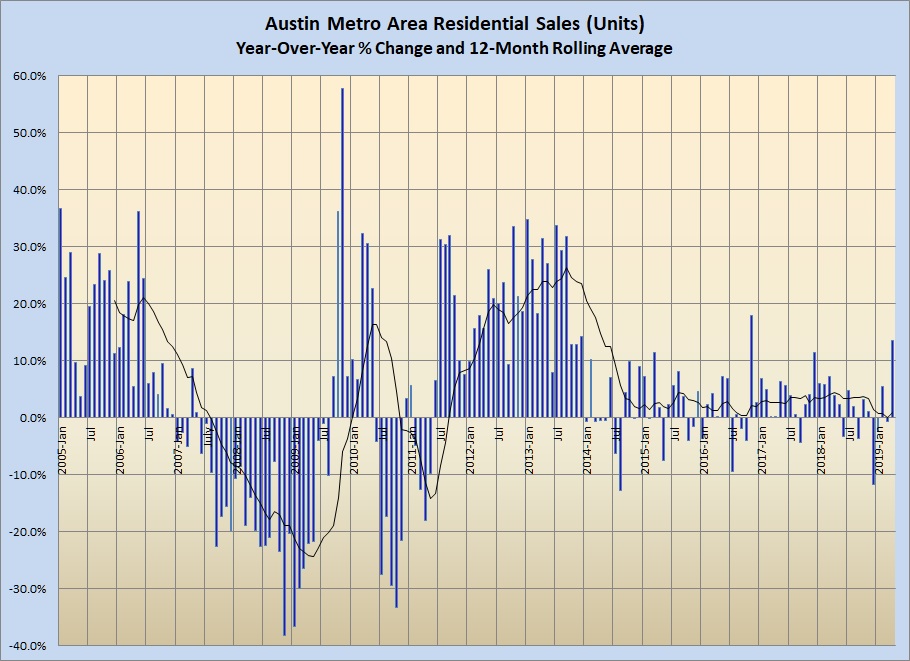

The average “odds of selling” for listings over the past 29-plus years was 26%. Since January 2013 it has been 41%! Notice the slope of the blue line at the right-most edge of the chart above and you’ll see that we’re not done yet.

On the other hand, both January and March unit sales in 2019 were slightly below the figures for the same months in 2018. Sales growth peaked from mid-2012 through 2013, and has moderated since then:

And year-over-year price increases have shown a fairly consistent trend for the past four years:

Again, demand is not the problem. We have a lot of new jobs being created and steady population growth. We simply don’t have enough homes to meet the demand, and the perceived price vs. value equation for many buyers got out of hand as a result.

I remain optimistic about continued growth in our residential real estate market for at least another year or two. We have a lot of work to do as a regional community to accommodate continued expansion — land use policies that will allow addition of housing where it’s needed and at a price point that meets buyers’ needs, transportation and mobility systems that allow those who don’t want or need to drive themselves everywhere to get out of their cars, and energy and utility infrastructure to make it all work. I believe we’ll see progress on regional policy in the coming year, but catching up with implementation will take years.

Discussion

No comments yet.