I have written a lot for much of the last year about the continuing shortage of housing for sale in the Austin area, noting that the pace of year-over-year price appreciation has slowed and that “days to sell” has increased somewhat in recent years. (Most recently 1st Quarter 2019 – Market imbalance continued and Days to Sell by Price Range.) Now I want to discuss my more comprehensive Market Dashboard looking back at the first three months of this year.

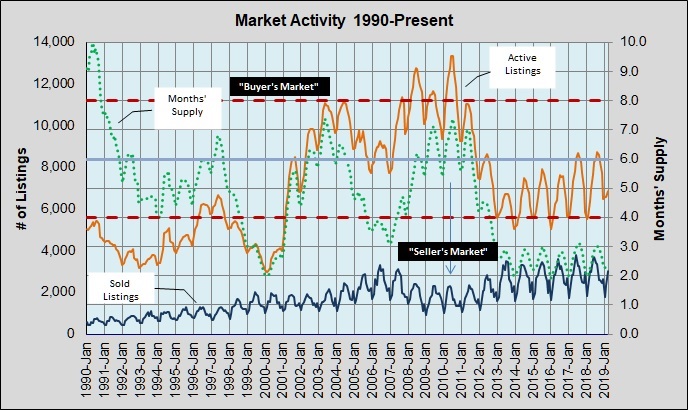

First, listing inventory remains very low, representing just 2.4 months’ supply, up slightly from the same time last year, but still less than half of a “balanced” supply:

Over the entire period graphed the average inventory for the Austin area was 4.7 months’ supply, but since January 2012, the year this cycle began, the average was 2.7 months. That’s just over half of the 5.3 months average for all the market cycles before this one in the last three decades.

With high demand and short supply come frustrated buyers. This chart shows the percentage of active listings that sold in each month during the same 29-plus years:

Prior to this cycle, the “odds of selling” had been above 50% for a total of 3 months and above 40% for 12 months. In the most recent 6 years and 3 months it has been 40% or higher for 42 months, and above 50% for 7 months!

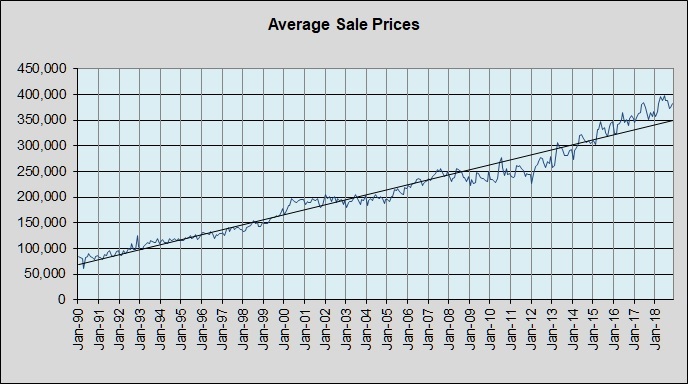

Through all of that, the trend for home prices has been surprisingly positive:

Seller’s markets push prices above the long-term trend-line, as you would expect, but look at the dot-com bust in 2001 and the mortgage crisis in 2008. The “great recession” affected several states very dramatically but in the aggregate, home prices in the Austin area leveled out instead of plummeting. (NOTE: Averages obscure extremes. There were certainly neighborhoods and sections of this metropolitan area that were hurt badly during those downturns, but even there price drops were fairly mild compared to places in California, Nevada, and Florida.)

So … what does 2019 have in store for us? I believe we’ll see continued short supply, but moderation in price appreciation compared to the early years of this cycle. Home builders will continue to increase the pace of new construction and may be able to relieve some of the pressure of continuing high demand. As long as growing employers and their employees want to move here and are willing to accept the challenges that come with fast growth, we may well have a couple more years ahead like the last couple. Buckle up!

Discussion

No comments yet.