My regular readers have seen the market dashboard that I have used over the past ten years or so, covering a variety of data from 1990 to present. In this post I will focus on 2017, with some comparisons to the last couple of market cycles.

First, it won’t surprise anybody who has been paying attention to know that home prices continued to rise in the Austin metro area last year:

Note that, not only have prices been going up in recent years, but also that in 2016 and 2017, they have been consistently above the long-term trend. The average sale price of a home (house, condo, or townhouse) across the 5-county metropolitan area reached a all-time high of $307,722 in December 2017. Very limited inventory of homes for sale is the reason for ongoing price pressure:

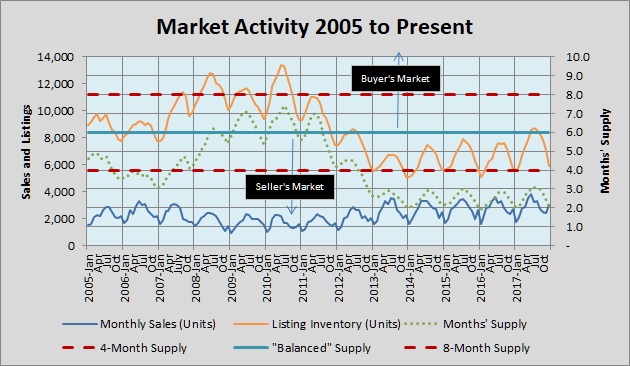

The dotted green line shows how long existing inventory will last at the current pace of sales. We have now completed five full years with inventory at or below half of what market economists consider a “balanced” supply (6 to 6 1/2 months’ supply) — the longest and most lopsided seller’s market we have ever experienced. And that results in competition among buyers for the limited supply. To put that into perspective, let’s use the long-term view:

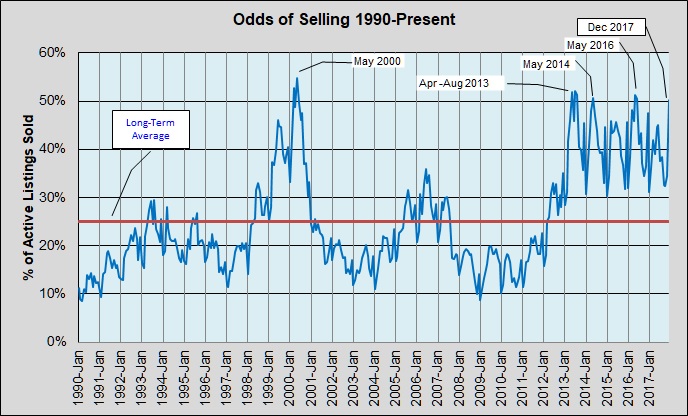

“Odds of Selling” means the percentage of active listings that sold each month. From January 1990 through December 2017, the “odds of selling” averaged 25%. Note this comparison:

- This metric reached 40% for the first time in May 1999 and stayed at or above that level for 12 of the next 16 months, going over 50% for 3 months in early 2000.

- The next time the “odds of selling” reached 40% was in March 2013. It has now been at or above 40% for 34 of the next 58 months, going to 50% or higher in 7 months over that time, including December 2017 (the only time that’s happened outside the traditional Spring/Summer selling season).

As I have commented previously, demand for housing in Austin and Central Texas is still being driven by real job creation and resulting population growth, not speculation by over-eager investors. Market cycles do happen, but I agree with most local market watchers that there is no reason to expect this market strength to be a “bubble” of the kind that burst in 2000 and 2006.

In some ways, we are in uncharted territory here, but most market watchers and local economists expect inventory constraints to remain with us in 2018, and for high demand to continue. Some geographic areas and price ranges will experience this differently, but it looks like another wild ride ahead this year. Will we see the market move toward “normal” in the future? Certainly, but so far it doesn’t look like it will be in 2018.

Discussion

Trackbacks/Pingbacks

Pingback: Austin Market Price Distribution | Bill Morris on Austin Real Estate - January 26, 2018

Pingback: Market Shift? | Bill Morris on Austin Real Estate - July 17, 2018