On Monday I tweeted a link regarding the most recent Clear Capital Market Report:

As always, this kind of report makes me curious about how the Austin/Central Texas real estate market compares. That’s the reason for this post.

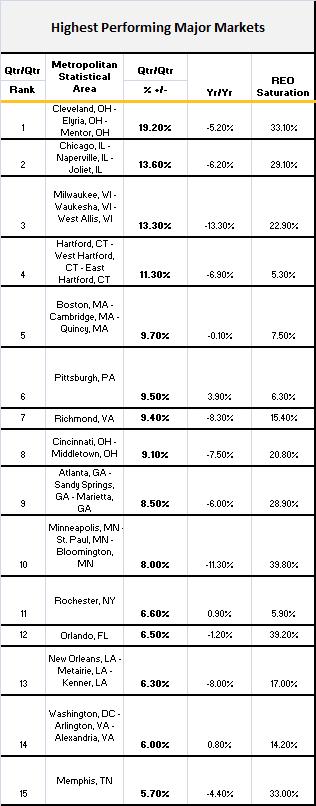

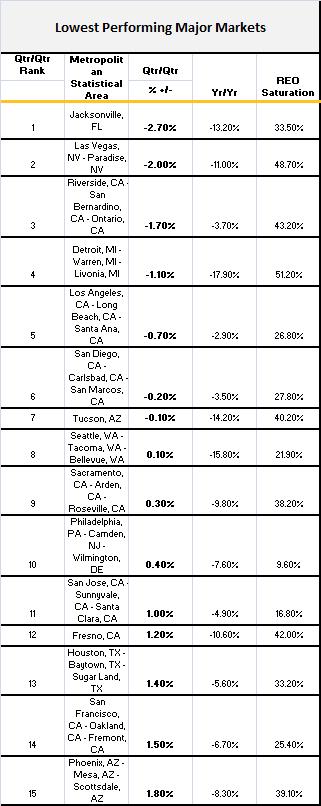

First, here are a couple of tables I lifted from the Clear Capital report (click to enlarge):

Interestingly, you will recognize that many of the cities on both lists — highest and lowest performing — have also appeared on lists of the cities that suffered most from the recession and housing downturn. It is encouraging to see real gains in home values using Clear Capital’s unique approach to quarter-to-quarter price comparisons, but many of these cities still have a long way to go before saying that home values have recovered. It is also very discouraging to see so many troubled cities still struggling, and posting losses in home values year-to-year. Clear Capital’s report notes that “The gains of summer are not recouping the longer-term declines, and national yearly home prices are down -6.2% compared to last year’s levels.”

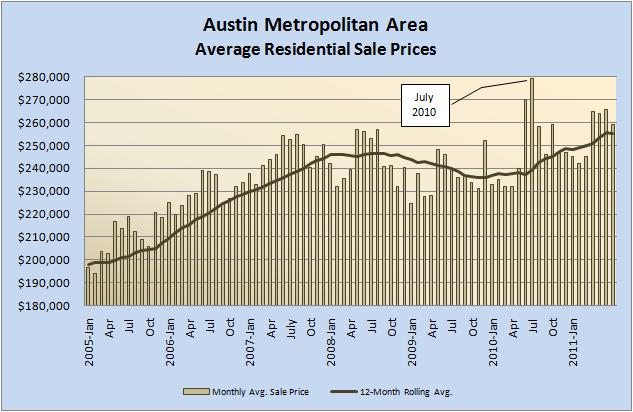

Clear Capital used data through August 2011. Final August data for Austin isn’t in yet, so I can’t make direct comparisons, but I can say that average home sale prices in May-June-July were 4.24% higher than in the previous three-month period (and unit sales were up more than 37%!). I can also say that the average sale price in July 2011 was 10% lower than one year earlier. As I have pointed out in the past, the average price in July 2010 was dramatically, and artificially, inflated because the tax credit program that ended the month before had shifted lower priced sales forward, leaving upper-end properties to dominate in July. I cannot comment knowledgeably about how much that distortion affects the year-to-year figures in the lists above, but I am confident that it is a factor. We did not have that kind of artificial influence this year, so the strength in sales and sale prices in Austin this spring and summer have been impressive:

A key influence on home values during this difficult period has been the proportion of distressed sales (short sales and foreclosures) in a local market area. Looking at the lists above, you will see that most of those metropolitan areas are still seeing huge numbers of foreclosed homes (REO Saturation) — 30% to 50% of all home sales! In contrast, 13.7% of homes sold in the Austin metropolitan area in May through July were foreclosures, and they tended to be concentrated in identifiable subdivisions and hyperlocal market areas. Distressed sales have not exerted the kind of generalized price pressure here that many other cities have experienced.

Summary: According to Clear Capital the healthiest quarterly gains in home values were in the Midwest 7.3%) and the Northeast (4.9%). Texas is in the South in their study, where quarterly improvement was 3.5%. The Austin area is above that average — using data only through July. Based on “raw” MLS data, expect to see final August prices higher than July, so our “apples to apples” comparison with these other cities should look even better. Moreover, Austin’s slow-but-steady growth is very refreshing given the upheaval still going on in so many other places.

Discussion

No comments yet.