Mortgage interest rates have been very, very low for most of 10 years now. Rumors have come and gone many times that rates would increase soon, raising concerns among prospective home buyers, and sometimes spurring short flurries of purchases. With news this week that the Federal Reserve has raised the “Fed Funds Rate,” we’ve already seen articles discussing the potential impact, including the possibility of rising mortgage rates.

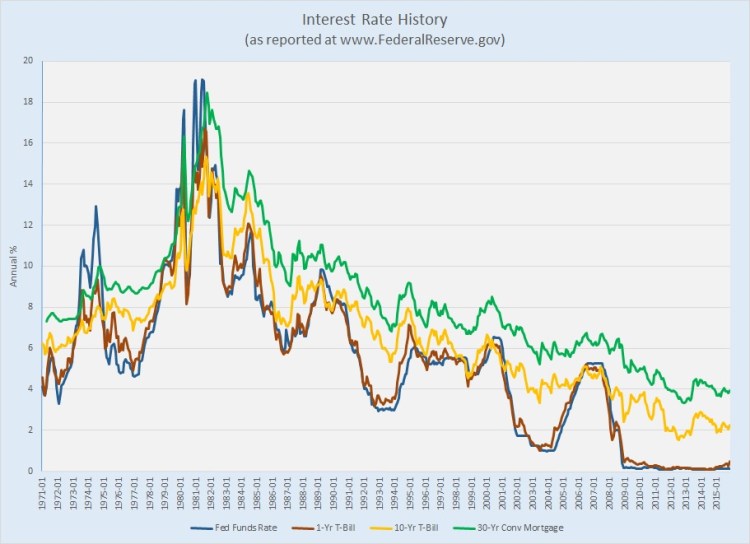

While higher mortgage interest rates are almost certainly in our future, the Fed Funds Rate will have little to do with them. In December 2015 I posted “All the talk about interest rates …” to point out that mortgage rates at that time were about half of the long-term average. That is still true today, even with some modest increases in recent weeks. In that post I also demonstrated that mortgage rates have rarely moved in tandem with the Fed Funds Rate, and in fact have sometimes moved in the opposite direction:

We have been spoiled, and younger home buyers have come to think of mortgage interest below 5% as “normal.” Is it NOT. As the health of the economy and the housing industry in general improve, there may be upward pressure on mortgage rates, and that is as it should be.

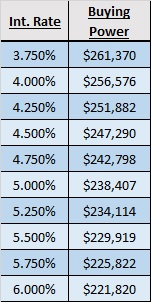

With that in mind, it is worth considering the impact higher interest will have on the “buying power” of prospective homebuyers. “More about interest rates — what can you buy?,” also in December 2015, included a couple of tables to illustrate that effect, including this one:

That table shows the price that a buyer qualified for a $1,600 monthly payment (PITI) could buy. I haven’t heard any forecast yet of rates going above 5% in the next year, but there are no guarantees. With that in mind, though, note that this hypothetical home buyer would lose about $18,000 in buying power if his or her qualifying rate moves from 4% to 5% — noticeable, but probably not catastrophic for most. In that same post, another table shows that the monthly payment for a $250,000 home would increase from $1,559 to $1,678 with the same change in the interest rate.

So, will mortgage rates change? Yes.

When? Hard to forecast, but watch the bond market, not the Fed.

Will sellers still sell and buyers still buy? Yes. That was true even with rates above 10% in the early 1980s, and it will certainly be true in the still-very low range to be considered in the coming year or two. The sky is not falling.

Discussion

Trackbacks/Pingbacks

Pingback: More on the Outlook for 2017 | Bill Morris on Austin Real Estate - March 17, 2017

Pingback: Interest Rates Rise | Bill Morris on Austin Real Estate - February 16, 2018