Reports on the United States residential real estate sector continue to disappoint, with weak housing starts, falling home sales, and declining prices. Even the Austin/Central Texas market experienced similar shifts in July 2011, but not as part of a trend as in other parts of the country. The Austin metropolitan area continues to enjoy population and job growth, high rental occupancies and resulting rising rents, and general strength in the regional economy.

To begin this month’s dashboard discussion, here is a snapshot of the Austin Metro market as of August 24, 2011:

Active Listings: 8,714

(down from 9,021 last month)

Sold Last 30 days: 1,753

(up from 1,644 last month)

Months’ Supply At That Pace: 4.97

(down from 5.5 months last time, and solidly in “sellers’ market” territory)

Pending Contracts: 2,550

(down from 2,698 last month)

Pendings at about 1 1/2 months’ sales indicates stable demand during the last month before the school year began here. It is worth noting that the final July market numbers used in the remainder of this summary reflect a decline in sales volume from June 2011 to July 2011 — not the increase seen in the most recent 30 days of MLS data. That is an indication of the volatility of the market over short periods of time, but supports the fact that underlying market strength remains. It is reasonable to expect some seasonal slowdown in the coming months, although homebuyer tax credits and general economic turmoil have so badly distorted seasonality over the past three years that predicting what “normal” will look like in 2011 is difficult.

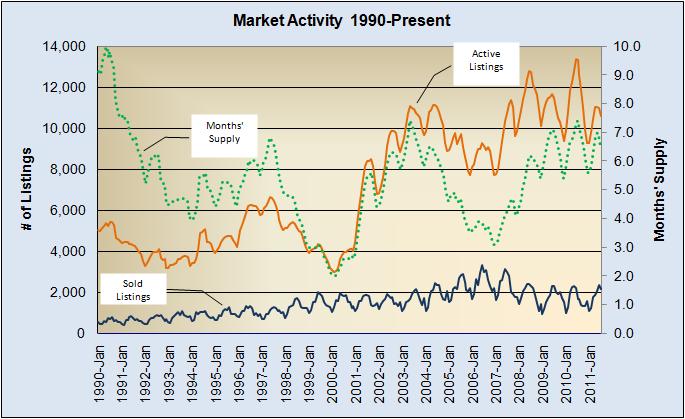

The continuing balance of supply and demand in the Austin housing market has served us well during this market cycle compared to some previous cycles — notably the last downturn that was driven directly by failures in the financial services industry, in 1989-1990:

The dotted green line shows the significant over-inventoried conditions in 1990, and the fact that even at the worst of the current cycle our listing inventory peaked at about 7 months. Focusing just on the 2005 to Present period shows how very well balanced this market has remained, especially since January 2009, our lowest month of unit sales in the cycle:

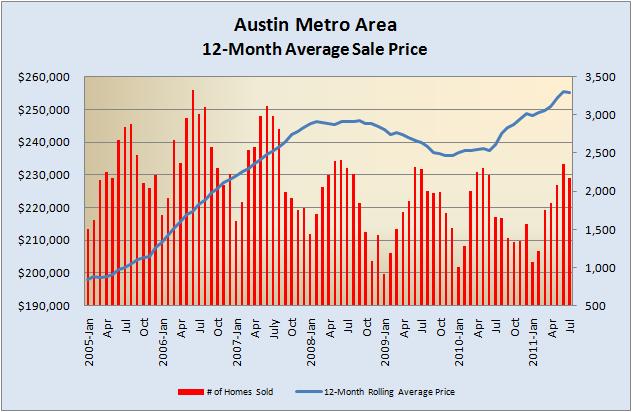

That balance has allowed preservation of property values, and a shift in the “mix” among home price ranges toward more expensive properties has raised average and median prices:

In July 2010, both average and median home sale prices spiked due to the end of the last homebuyer tax credit program — with very few first-time buyers left in the market and more expensive move-ups dominating sales. July 2011 prices were well below that level, but still supporting the years-long upward trend.

Using the 12-month moving average sale price filters out month-to-month and seasonal volatility. This chart provides that view, coupled with monthly actual sales:

Unit sales volume is clearly far below the pre-recession levels of 2006 and 2007, but month over month sales growth this year has been impressive — and without tax incentives to create temporary demand. Moreover, the price mix this year represents more normal market performance than 2009 or 2010.

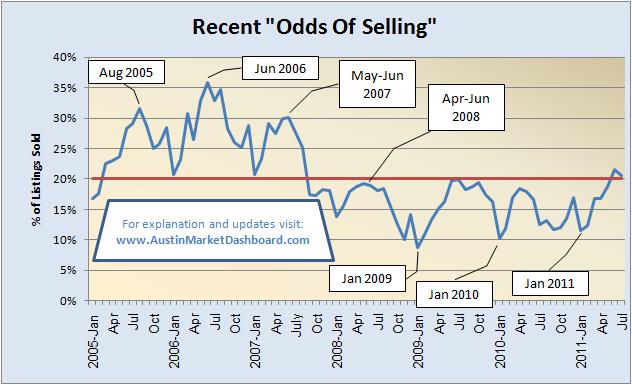

Finally, another view of market absorption is encouraging. Since 2005, on average, 1 out of 5 active listings have sold each month. That ratio has been as high as 36% (June 2006) and as low as 9% (January 2009). Note the wild gyrations in this number from late 2008 to July 2011:

In all market cycles since 1990, one or two dips to about 10% “odds of selling” signaled the beginning of a new market growth cycle. This time, we have touched that bottom three times, but in June 2011 we exceeded the multi-year average for the first time since the housing downturn reached Austin. Even with a monthly decline in sales in July, sales still absorbed 21% of active listings.

There is every reason to expect some seasonal softness in unit sales and prices in the coming months, but as I mentioned at the outset the Austin/Central Texas economy remains resilient. Economic strength continues to attract employers and employees to move here, that trend is filling available rental space and pushing rents upward, and as those new Austinites either sell homes elsewhere or just gain confidence in their futures they become Austin-area homeowners. Economic forecasters predict Austin’s strength to continue for many years.

The links below will display printable versions of the entire Austin Market Dashboard:

You’ll also find frequent market news updates on my personal website (BuyOrSellAustin.com) and comments at BillMorrisRealtor.com. I invite you to check in with me there, follow me on at Twitter.com/BMorrisRealtor and “like” me on Facebook. Also feel free to contact me directly whenever I can be of service.

Discussion

No comments yet.